This post was originally published on this site.

“It’s a market of stocks, not a stock market” is an old cliché, intended to remind us why investing is ultimately about how well individual companies are doing from the bottom up and not a top-down view of the FTSE 100 or S&P 500.

I don’t entirely agree with this thinking, at least in the modern world. The growth of index investing has meant that many people now invest in the whole market or in broad sectors and don’t care about the companies they hold. Money flowing in and out of funds can do more to determine whether valuations rise or fall than real changes in a business’s fundamentals.

Sign up to Money Morning

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

(Image credit: Factset)

The year-over-year blended growth rate (ie, including both results reported so far and latest estimates) for the S&P 500 is currently 15.1%, according to FactSet – the sixth successive double-digit quarter. The index is expensive: at just over 7,100, it’s on a trailing price/earnings ratio of 28. Yet if earnings keep compounding like that, it’s not really a stretch to stay bullish.

The greatest threat to earnings growth

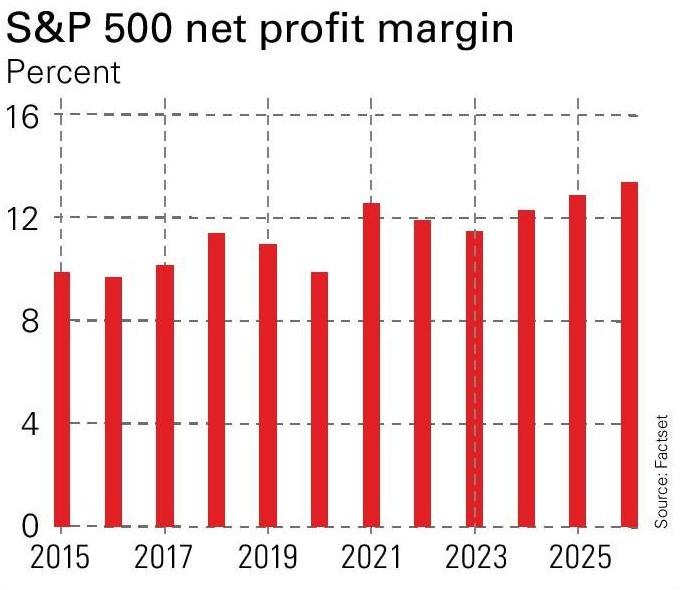

In the medium term (maybe three to five years), one has to wonder whether giant companies can continue to earn such high margins: the S&P 500 net margin is once again setting a new record of 13.4%. The geopolitical and political trends that let businesses – especially multinationals – become ever more profitable over several decades are shifting. Maybe this goes into reverse. But a few years is a lifetime in the markets and we are obviously not there yet.

In the shorter term (maybe a year or two), the extent to which AI mania is underpinning this boom cannot be ignored. In the tech sector, earnings growth is at 46%. There is a very fine line to be walked here: if all this investment does not bring huge productivity gains, it will grind to a halt. If it puts too many people out of stable employment, the political backlash could be equally dangerous. Yet all investors care about is what will happen in the next couple of quarters, and there is no sign of the boom letting up so far.

So what is the greatest ultra-short-term threat? Energy. The amount of oil at sea when the Middle East crisis started means that the consequences of the closure of the Strait of Hormuz and the shutting in of millions of barrels a day of crude is not really translating into shortages yet. Even if supplies resume tomorrow, there will be a lag and the effects will still show up over the next couple of months. But if they do not resume soon, the crunch is going to become very evident. A market focused on historic earnings and understandably upbeat forecasts is not pricing that in.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.

Explore More

{kind=link}