This post was originally published on this site.

Korea is still an emerging market, or so MSCI reckons. On Tuesday, the most important provider of global indices – the MSCI World and the MSCI Emerging Markets matter much more than the equivalents from FTSE Russell and S&P Dow Jones – once again declined to put it on the watch list for upgrade to developed status.

On one hand, this situation feels increasingly ridiculous. Korea is a very advanced, high-tech economy, home to key tech players such as Samsung Electronics and SK Hynix. GDP per capita measured at purchasing power parity is higher than the UK, France, Japan and many other heavyweights. How can this be an emerging economy in any meaningful sense?

Yet there are aspects to Korea that feel like an emerging market. The ones that MSCI cites are certain limitations that bother institutional investors (restrictions on trading the Korean won offshore is a key one) – although FTSE Russell has classed Korea as developed since 2009, so the importance of these is not cut and dried.

Sign up to Money Morning

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don’t miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

However, perhaps more significant for the long-term future of the Korean stock market is the dominance of large business conglomerates (chaebols), of which the Samsung group is the biggest. The founding families of these groups still control them – often using a series of shareholdings between different listed entities – and frequently make decisions for their own benefit to the disadvantage of minority shareholders.

Generational changes are happening in Korea

Corporate governance is a major reason for the “Korean discount” – the fact that Korean stocks trade at lower valuations than peers elsewhere – but there are signs that this is changing. Policymakers have been pushing reforms, inspired by what governance changes in Japan have done for that market, with some success.

(Image credit: MSCI Korea index)

Generational changes also mean a structural shift in attitudes is inevitable, suggested a Korea manager at a recent conference. The individuals who built up chaebols in the 1960s and 1970s put huge importance on passing on control to their heirs as cheaply as possible (Korea has very high inheritance tax). They are now largely dead, the handovers are being completed, and tax bills are being settled. Their heirs will have different priorities that may often be better served by unlocking the full value of their businesses.

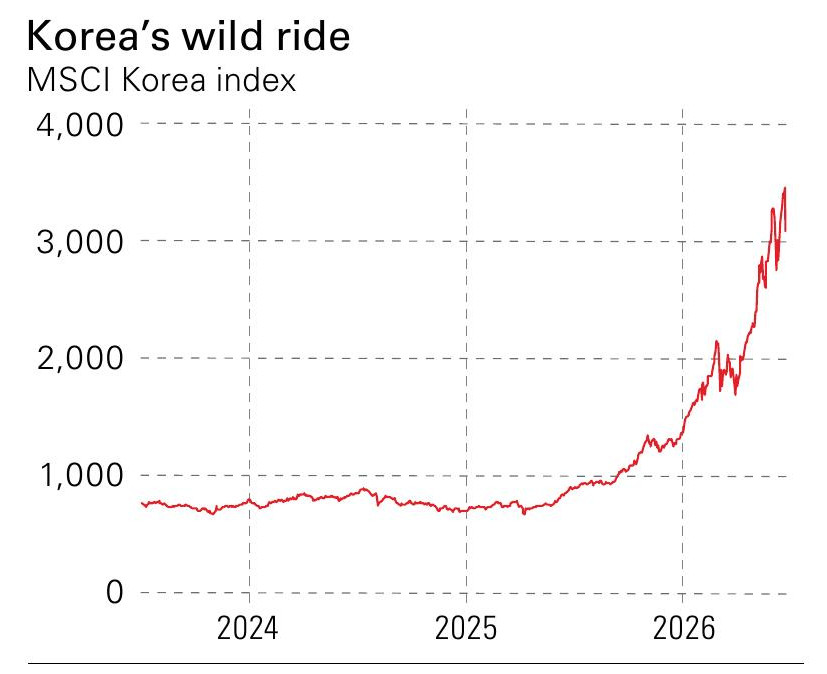

So the bull case for Korea sounds easy to make. It does not depend on MSCI one day acceding to the obvious, although being added to the developed index would result in significant inflows from tracker funds. And on the face of it, Korean stocks look very cheap – the MSCI Korea stock market index is on a forecast price/earnings ratio (p/e)of eight.

Yet this reflects the huge weight in Samsung and SK Hynix (65% combined) and how fast they are expected to grow. The MSCI Korea Equal Weight is on a forward p/e of 15, which is not cheap. Most of all, note the market is up by 260% in won terms in a year. If the AI boom continues, it will go higher, but have no illusions. Right now, a Korea stock market tracker is not a valuation play or a reform play – it is entirely an AI play.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.

Explore More

{kind=link}